Deciding between Original Medicare and the Medicare Advantage program is an important first decision everyone needs to consider once they start their Medicare coverage. The two programs are completely different in how they are structured. Your ability to access either program, personal health considerations, preference for either a fixed monthly budget or a variable monthly budget and the associated higher or lower premiums and access to doctors and/or hospitals can help determine which program you should use. Let’s compare the two programs and list the pro’s and con’s of each.

Enrollment Considerations:

When you’re Medicare Part B first becomes effective you have a one-time opportunity to enroll into either Original Medicare with a Medicare Supplement and Prescription Drug Plan or enroll in a Medicare Advantage plan without having to answer health questions. This is your only opportunity to access any program available without being underwritten for health.

After your first enrollment period any changes to your Medicare Supplement plan requires you to answer health underwriting questions. The Medicare Advantage plans and prescription drug plans allow you to switch between plans once a year without having to go through medical underwriting. So, the Medicare Advantage plans and Prescription Drug plans are flexible and allow you to switch your coverage once per year during Annual Enrollment Period the Medicare Supplements can be changed anytime throughout the year pending you can pass medical underwriting.

Personal Health Considerations:

If you see several specialists or have some major health concerns it might be beneficial to go with a Original Medicare. On that plan you have the fixed premium costs of your Supplement and Prescription Drug plan but potentially very little out of pocket costs after that for doctor and / or hospital charges. For example, a Medicare Supplement plan G

has covers everything but the Part B deductible which is only $198 for 2020. Meaning after you meet that expense all Medicare approved charges would be covered.

Since the Medicare Advantage program typically has much lower monthly premium (several plans offer $0 monthly premiums) the costs for your health coverage are offset by potentially higher maximum out of pocket costs for the plans. In Indiana the maximum out of pocket for the plans is between $3,700 – $10,000 depending on the plan.

If you are healthy you are a great candidate for either program and should think through all of the considerations. However, if you do use medical services often then you might be better off paying the premium and limiting your out of pocket costs.

Preference for Fixed or Variable Monthly Budget:

Similar to what is stated above, the Original Medicare plan has more premium per month and potentially very little out of pocket when compared to the Medicare Advantage plans. Typically, the premiums are about $1300 – $2500 per year depending on age, gender and tobacco usage. Out of pocket costs for a plan G is $198 for 2020. Prescription co-pays vary depending on which prescription you are on.

Other people prefer to go onto a Medicare Advantage plan and have lower monthly premium cost knowing that if they get sick they can potentially spend more money out of pocket for the services that they used with their Medicare Advantage plan. Typically, the Medicare Advantage plans are $1,500 – $2,500 less in premium per year than the Original Medicare supplement and Prescription Drug plan premiums but have out of pocket maximums between $3,700 – $10,000 per calendar year.

Consider both the differences in premium between the plans and the potential differences in out of pocket costs to see which fits better for you. Some people prefer to have a budget with more fixed costs that they can plan on and go with the Original Medicare knowing that if they get sick there would be potentially little out of pocket costs. Other people prefer to save monthly on their premium expenses and are willing to pay co-pays when they use the services.

Access to doctors / hospitals:

Original Medicare is accepted by about 96% of doctors across the country. Of the 4% that don’t accept Medicare assignment, most of those doctors will still accept Medicare patients. Medicare Advantage plans are typically either PPO’s or HMO’s so the amount of doctors in network is typically much lower.

If you are going with a Medicare Advantage plan it is important to check that your doctors and preferred hospital networks are in network. This can save you a lot of extra money and expenses by using “out of network” physicians.

If being able to travel widely and see any physician you would like is a major concern, perhaps going with Original Medicare would be better for you.

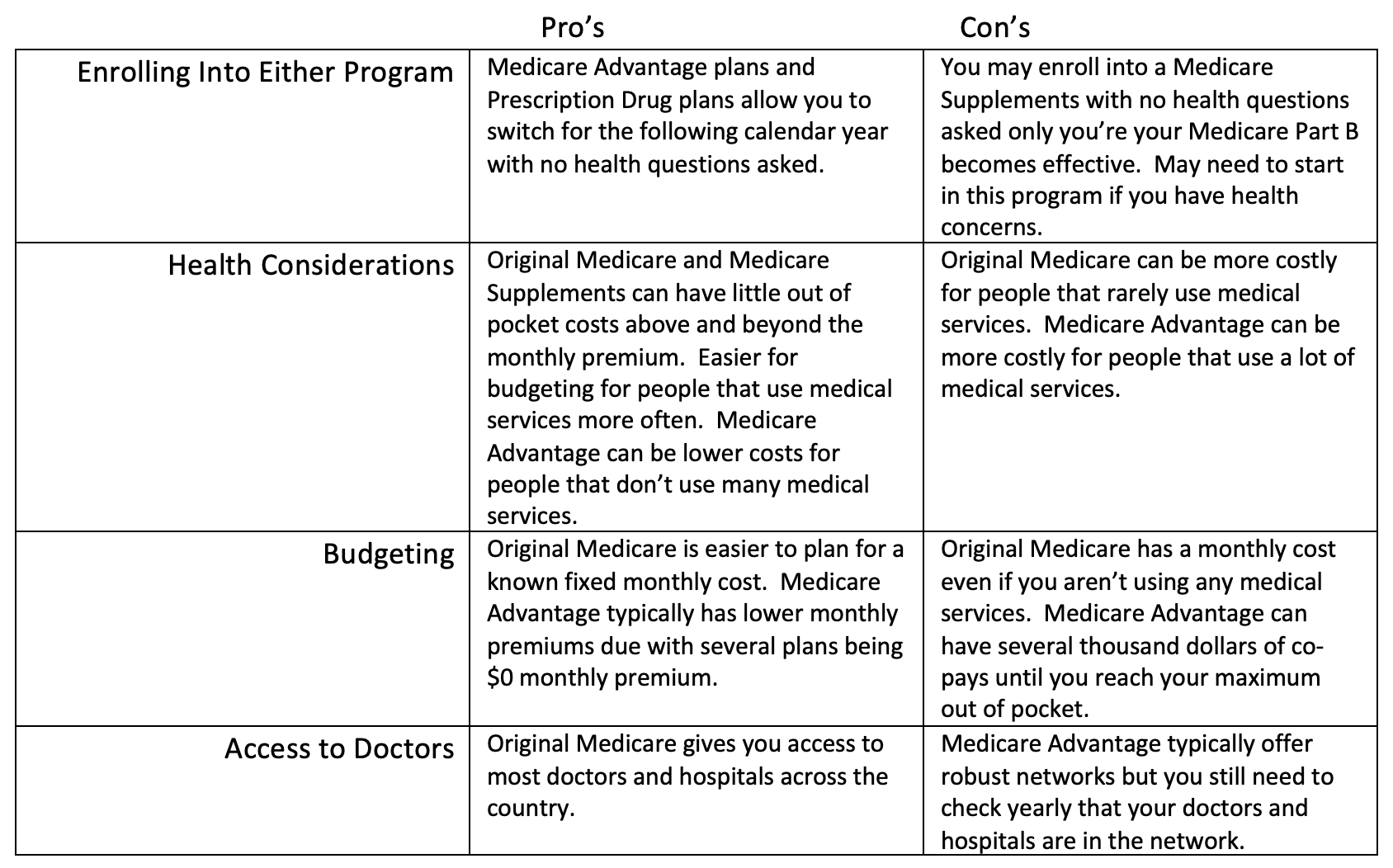

In Summary here’s a little chart of the Pro’s and Con’s of each:

I hope this summary helps you decide which program – Original Medicare or Medicare Advantage is better for your situation.

IF YOU NEED ADVICE OR HELP

If you have any questions or want professional advice for your situation please call, email or text us and we’ll be happy to advise and assist you. We are professional Medicare shoppers contracted with the insurance carriers so that we can work for you for FREE.

By representing just about every insurance company around we can be sure to find you the best coverage for your needs. The insurance companies pay us to help you find the best plan, enroll into that plan and provide ongoing service to you.

LINKS

Here is the link to find a local Social Security office: https://www.ssa.gov/locator/

The website to apply online for Medicare benefits: https://www.ssa.gov/benefits/medicare/

The phone number to sign up for Medicare over the phone is 800-772-1213.Here is their contact website: https://www.ssa.gov/agency/contact/phone.html

Jason Newby, CEO

Keys To Medicare

Jason has been helping people shop for Medicare Supplements or Medicare Advantage plans for almost 20 years. A nationally recognized agency, Keys To Medicare, helps you understand the pro’s and con’s of the coverages available to make sure you get the best coverage for your situation. In addition to helping you sign up, we do annual reviews to make sure you continue to have the best coverage possible.